9 April 2026 · 6 min read

The Financial Companion You Don't Have Yet

Why the future of financial services needs a sherpa, not a product catalogue

Most people think a sherpa is a guide who takes you to the top of the mountain. That is only part of the story. The Sherpa people live in the Himalayan mountains, but in the Western world they are best known as expedition companions, which is why the ethnic name is so often used as a job title.

A team of high-altitude sherpas includes at least six distinct roles. The sirdar coordinates the entire operation. The route-builder goes weeks ahead of everyone else, fixing ropes and ladders across crevasses, constructing the path before anyone can use it. The climbing sherpa walks beside you step by step, carrying the load when you cannot. And while expedition companies sell expensive summit packages, the sherpa's personal philosophy on the mountain is different. He is not there to get you to the top. He is there to bring you back down alive.

This is the best analogy I have found for where financial services should be heading.

The problem with products

The entire financial services sector today is built around products. The customer has a bank account, a mortgage, a second and hopefully third pillar pension, life and home insurance, a personal investment portfolio. Each product is often sold by a different institution, managed on a different platform, and regulated under different legislation. The customer sits in the middle of all this, expected to cope on their own, often entirely alone with their financial affairs.

This logic worked when these products were genuinely separate businesses. Banking dealt with payments and lending. Insurance with risk pooling. The pension sector with long-term savings. But the boundaries between products have blurred over time. A mortgage is simultaneously borrowing, insurance (what happens if I lose my job?), investment (property as an asset), and pension planning (will I own my home when I retire?). One decision touches four financial sectors that rarely communicate with each other.

The customer, however, does not usually think in products. Nobody wakes up thinking "I need an insurance-based investment product with a guaranteed minimum return." People think: can I afford that flat today? Will my children get a good education? What happens if I fall ill? Will I have enough savings if I become unable to work? What if I can no longer manage a full-time job physically?

These questions essentially fall into four life domains: housing, education, healthcare, and end of life. Financial products are practical tools for addressing important life questions, not ends in themselves.

This does not mean one financial services provider should do everything. But for the customer, different services from different providers should form a single, coherent whole.

Sherpa roles in financial services

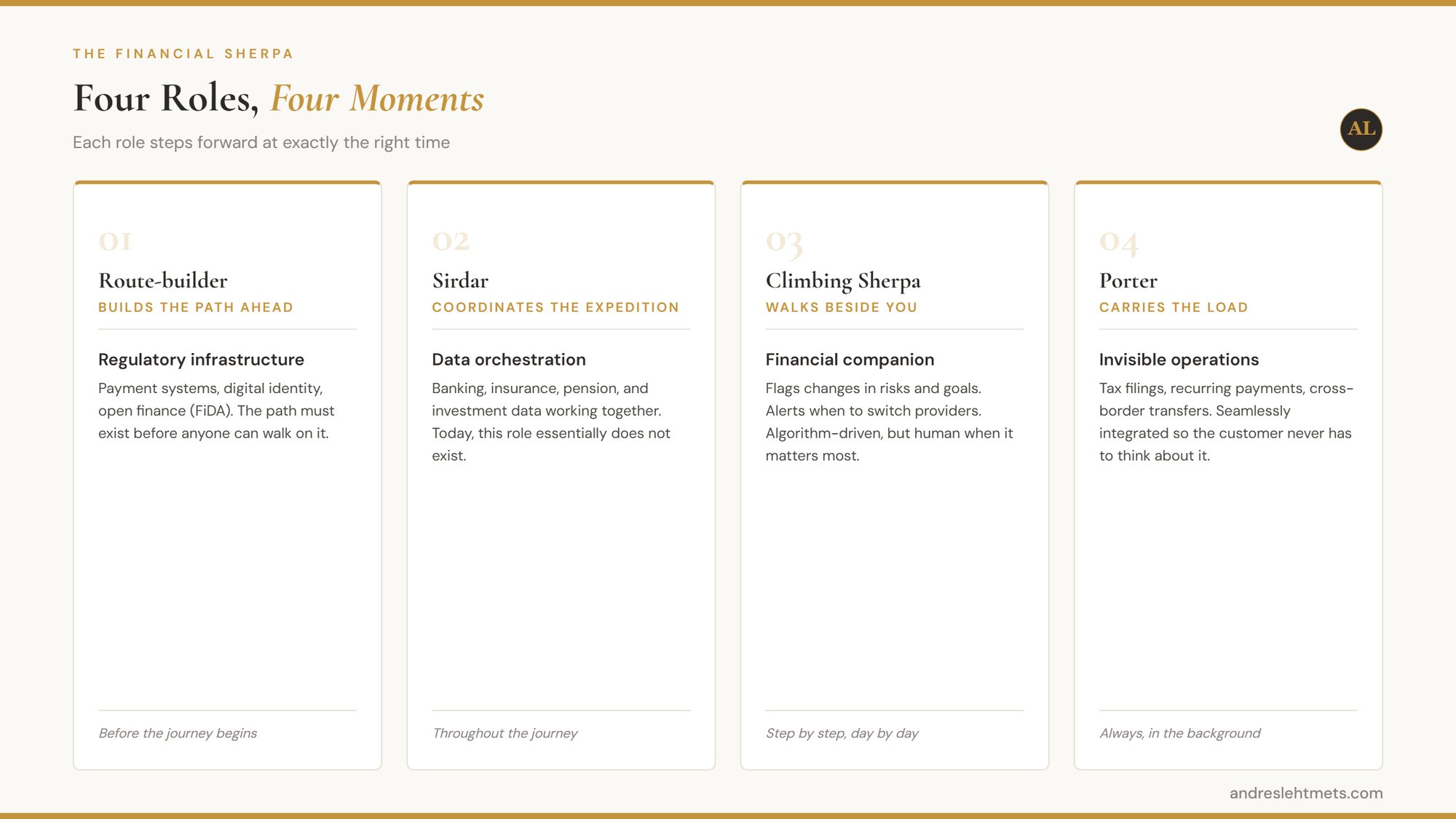

The strength of the model sherpas offer is that it is not one role but several. Most importantly, each role steps forward at exactly the right moment.

The route-builder constructs the path before the climber even starts. In financial services, this is the regulatory framework, financial supervision, and infrastructure: payment systems, digital identity verification, open data sharing (open banking and open finance). The path must be built before anyone can walk on it.

The sirdar coordinates the entire expedition. In financial services, this means maintaining the big picture: banking, insurance, pension, and investment data must work together, not against each other or in isolation. Today, this role essentially does not exist.

The climbing sherpa walks beside you, step by step. This is the day-to-day financial companion. This part of the service flags changes in risks, goals, and spending habits (when the client gives explicit consent) and alerts you when it makes sense to switch providers. In the future, services will be increasingly algorithm-driven, but human contact must remain where it is needed most.

And the porter: sometimes you simply need someone to take the tedious part off your hands. The customer should not have to think about managing services every day. Tax returns and recurring payments are seamlessly integrated into daily life, and global cross-border payments work around the clock at a reasonable cost.

The key point is this: nobody wants their financial services provider living on their shoulder every day. The customer wants them to be there exactly when needed. Like a good sherpa. Always present, but never intrusive. Invisible when appropriate, yet ready to respond quickly. Aware of the client's wishes and, more importantly, their capabilities. Expert, but not condescending. This is precisely where most financial institutions get it wrong today. Providers are either completely absent (you only hear from your insurer when it is time to renew) or annoying (endless one-sided generic advertisements for products the particular customer does not actually need).

What has to change

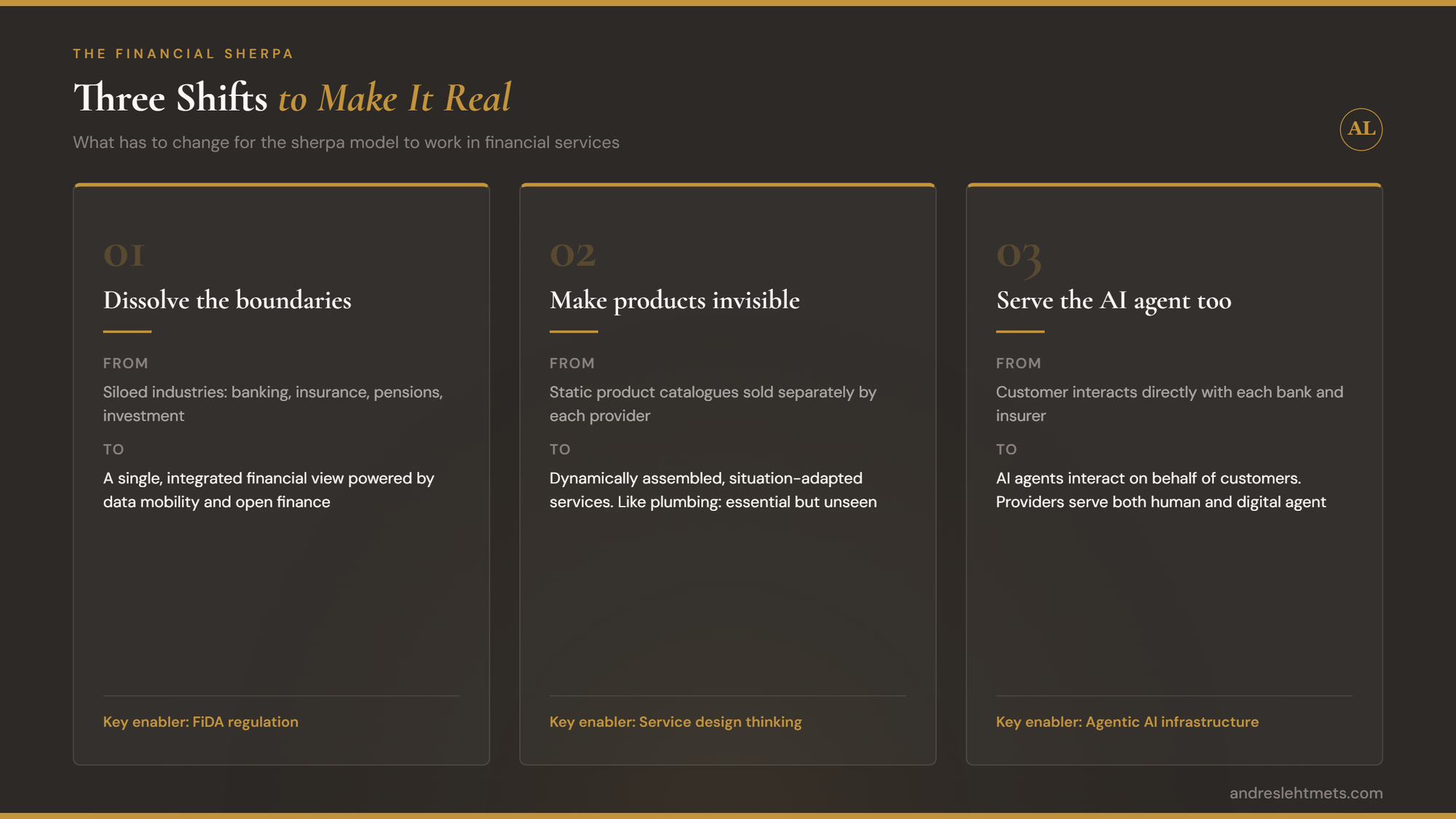

Three things need to happen for the sherpa model to become a reality in the financial world.

First, the boundaries between financial services need to disappear. As long as banking, insurance, pensions, and investment are viewed separately, a financial companion cannot emerge. The key lies both in service design and in data mobility. This is precisely why the Financial Data Access regulation (FiDA), currently being negotiated in the European Union, is so important.

FiDA is not an isolated initiative. It forms part of the broader EU digitalisation agenda that began with the European strategy for data in 2020, which gave impetus to the creation of common European data spaces across sectors, including finance. In November 2025, the Commission adopted the EU Data Union strategy to scale up access to data for artificial intelligence, streamline data rules as part of the simplification agenda, and safeguard European data sovereignty. Scaling up and interconnecting these common data spaces remains central to building a single market for data in the EU, and that market would not be complete without access to financial data. FiDA is the prime building block for the financial data space.

Crucially, FiDA should not be understood as a zero-sum game that pits data users against data holders. In the digital age, no financial services provider can afford to ignore the potential of data-driven business models. Under FiDA, data holders will also have the right to access customer data held by others, subject to customer permission, meaning they can become data users themselves and reinforce their own competitive edge. Many market participants across the EU are already preparing for open finance, seeing it as both inevitable and an opportunity for innovation.

For the consumer, the implications are significant. FiDA creates the legal foundation for customer financial data to be visible to all providers, if the customer so decides. Without this data mobility, the sherpa is blind. When data moves freely with the customer's consent, switching costs and barriers to market entry decrease. New and smaller providers can compete not on data volume, but on service quality and fit. The result is more personalised services: not the same standard package for everyone, but solutions tailored to individual circumstances.

Second, product-based thinking needs to go. Products will not disappear, but they should become invisible. The customer does not think about plumbing when turning on the tap. Financial services should work the same way: dynamically assembled, adapted to the situation, and changing as circumstances evolve.

Third, the development of Artificial Intelligence, and AI agents in particular, will transform the entire relationship between customer and provider. Today, the customer interacts with their bank and insurer. Tomorrow, an AI agent will partly interact on the customer's behalf: managing cash flows, comparing policies, even executing transactions. The financial services provider will then need to serve both the customer and their digital agent, while knowing precisely when human contact is necessary.

Coming down the mountain is harder than going up

Sherpas celebrate with you when you reach the summit. And then they help you get back down, which is statistically more dangerous than the ascent.

In the financial sector, people love to celebrate the sale: congratulations on your new mortgage; thank you for taking out your policy with us; welcome to your new investment. But the real value lies in what comes after. Managing the mortgage when interest rates change. Adjusting the policy when your life changes. Rebalancing investments when markets move.

The best sherpas are known not for getting people to the summit, but for getting them home. And when everything goes well, something happens that no advertising campaign can achieve: the climber embraces their sherpa, leaves a tip, and recommends them to the next expedition team. The best financial services providers will become known not for their products, but for their outcomes. And the best marketing is a satisfied customer who tells their friends about you.

The shorter version of this article was originally published in Estonian biggest business newspaper Äripäev.

Andres Lehtmets

Independent advisor on financial regulation and digital innovation. Former Senior InsurTech Expert at EIOPA. Research Analyst at Cambridge Centre for Alternative Finance. Writing weekly for 4,700+ professionals.